The Law Accompanying the 2020 Budget, Law 5/2020, of April 29, has recently been published in the Official Journal of the Generalitat of Catalonia (DOCG), which includes relevant tax changes, especially concerning the Personal Income Tax (“IRPF”), the Inheritance and Gift Tax (“ISD”) and the Transfer Tax (“ITP”).

- Regarding the Personal Income Tax (IRPF), the increase in the minimum per taxpayer stands out in those cases in which the general and savings taxable gross bases, together, do not exceed € 12,450; a new section is introduced on the regional scale (from now on the marginal rate will be 23.5% for taxable net bases above € 90,000 and 24.5% from € 120,000). The maximum autonomous marginal rate of 25.5% (which together with the state scale implies a marginal rate of 48%) is maintained. All with effects for 2020.

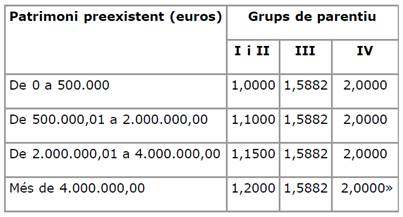

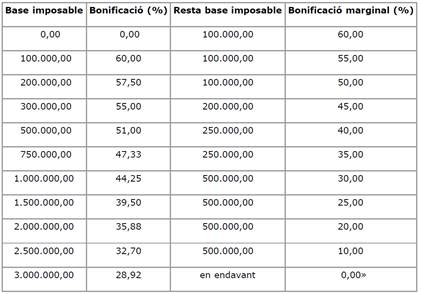

- Regarding the Inheritance and Gift Tax (ISD), it should be noted that new multiplying coefficients are introduced for kinship groups I and II, to which a coefficient of 1.1, 1.15 or 1.2 will be applied, in case the pre-existing patrimony of the beneficiary is greater than € 500,000, € 2 million or € 4 million, respectively. Previously, the multiplier coefficient was 1 regardless of the beneficiary’s pre-existing assets; On the other hand, the reduction of the quota for heirs of Group II is reduced, so that the scale of discounts will go from being 99% -20% of the tax payable to being 60% -0%. Both measures represent a relevant increase in ISD taxation, especially for Group II taxpayers. These modifications take effect from May 1, 2020. See attached the tables of multiplier coefficients and bonuses for Group II taxpayers after the modifications explained.

- Regarding the Transfer Tax (ITP), in its TPO modality, the discount of the fee for the transmission of homes to real estate companies is modified (from now on there is a time limit of 3 years to resell the home, instead of 5); a reduced rate of 5% is introduced for home purchases by single-parent families; for the Stamp Duty (AJD), a 100% discount is included in the tax payable for public deeds of a constitution in the case of parcel horizontal property regime. All this with effect also from May 1, 2020.

If you have any questions regarding inheritance tax in Spain, contact GM Tax tax advisors by telephone or email.